AlgoBuilder [Mean-Reversion] | FractalystWhat's the strategy's purpose and functionality?

This strategy is designed for both traders and investors looking to rely and trade based on historical and backtested data using automation.

The main goal is to build profitable mean-reversion strategies that outperform the underlying asset in terms of returns while minimizing drawdown.

For example, as for a benchmark, if the S&P 500 (SPX) has achieved an estimated 10% annual return with a maximum drawdown of -57% over the past 20 years, using this strategy with different entry and exit techniques, users can potentially seek ways to achieve a higher Compound Annual Growth Rate (CAGR) while maintaining a lower maximum drawdown.

Although the strategy can be applied to all markets and timeframes, it is most effective on stocks, indices, future markets, cryptocurrencies, and commodities and JPY currency pairs given their trending behaviors.

In trending market conditions, the strategy employs a combination of moving averages and diverse entry models to identify and capitalize on upward market movements. It integrates market structure-based moving averages and bands mechanisms across different timeframes and provides exit techniques, including percentage-based and risk-reward (RR) based take profit levels.

Additionally, the strategy has also a feature that includes a built-in probability function for traders who want to implement probabilities right into their trading strategies.

Performance summary, weekly, and monthly tables enable quick visualization of performance metrics like net profit, maximum drawdown, profit factor, average trade, average risk-reward ratio (RR), and more.

This aids optimization to meet specific goals and risk tolerance levels effectively.

-----

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

Trading:

1. Trading:

- Designed for traders looking to capitalize on bullish trending markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for active trading with a focus on mean-reversion and risk per trade approach.

◓: Mode | %: Risk percentage per trade

3. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully investing in the asset during bullish conditions.

- ◓: Mode | %: Risk not applied (In investing mode, the strategy uses 10% of equity to buy the asset)

-----

What's is FRMA? How does the triple bands work? What are the underlying calculations?

Middle Band (FRMA):

The middle band is the core of the FRMA system. It represents the Fractalyst Moving Average, calculated by identifying the most recent external swing highs and lows in the market structure.

By determining these external swing pivot points, which act as significant highs and lows within the market range, the FRMA provides a unique moving average that adapts to market structure changes.

Upper Band:

The upper band shows the average price of the most recent external swing highs.

External swing highs are identified as the highest points between pivot points in the market structure.

This band helps traders identify potential overbought conditions when prices approach or exceed this upper band.

Lower Band:

The lower band shows the average price of the most recent external swing lows.

External swing lows are identified as the lowest points between pivot points in the market structure.

The script utilizes this band to identify potential oversold conditions, triggering entry signals as prices approach or drop below the lower band.

Adjustments Based on User Inputs:

Users can adjust how the upper and lower bands are calculated based on their preferences:

Upper/Lower: This method calculates the average bands using the prices of external swing highs and lows identified in the market.

Percentage Deviation from FRMA: Alternatively, users can opt to calculate the bands based on a percentage deviation from the middle FRMA. This approach provides flexibility to adjust the width of the bands relative to market conditions and volatility.

-----

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

This comparison filter can be turned on (>) or off.

For example, you can set the filter so that MA#1 > MA#2, meaning the first moving average must be above the second one before the script looks for entry conditions. This adds an extra layer of trend confirmation, ensuring that trades are only taken in more favorable market conditions.

⍺: MA Period | Σ: MA Timeframe

-----

What entry modes are used in this strategy? What are the underlying calculations?

The strategy by default uses two different techniques for the entry criteria with user-adjustable left and right bars: Breakout and Fractal.

1. Breakout Entries :

- The strategy looks for pivot high points with a default period of 3.

- It stores the most recent high level in a variable.

- When the price crosses above this most recent level, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot high left bars period | ◨: Pivot high right bars period

2. Fractal Entries :

- The strategy looks for pivot low points with a default period of 3.

- When a pivot low is detected, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot low left bars period | ◨: Pivot low right bars period

2. Hunt Entries :

- The strategy identifies a candle that wicks through the lower FRMA band.

- It waits for the next candle to close above the low of the wick candle.

- When this condition is met and the bar is closed, the strategy takes the buy entry.

By utilizing these entry modes, the strategy aims to capitalize on bullish price movements while ensuring that the necessary conditions are met to validate the entry points.

-----

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

Initial Stop-Loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14).

Example - ATR (14) * 2

⍺: ATR period | Σ: ATR Multiplier

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

Example - ADR (20) * 2

⍺: ADR period | Σ: ADR Multiplier

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

Application in Strategy (ATR/ADR):

- The strategy calculates the current bar's ADR/ATR with a user-defined period.

- It then multiplies the ADR/ATR by a user-defined multiplier to determine the initial stop-loss level.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

-----

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

Example:

If the entry price is $100, the initial risk is $10, and the RR ratio is 2, the break-even level is $100 + ($10 * 2) = $120.

FRMA Based:

Moves the stop-loss to break-even when the price hits the FRMA level at which the entry was taken.

Calculation:

Break-even level = FRMA level at the entry

Example:

If the FRMA level at entry is $102, the break-even level is set to $102 when the price reaches $102.

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

When Both Percentage (%) Based and RR Based Take Profit Levels Are Off:

The script will adjust the take profit level to the higher FRMA band set within user inputs.

Calculation:

Take profit level = Higher FRMA band length/timeframe specified by the user.

This ensures that when neither percentage-based nor risk-to-reward-based take profit methods are enabled, the strategy defaults to using the higher FRMA band as the take profit level, providing a consistent and structured approach to profit-taking.

For TP1 and TP2, it's specifying the price levels at which the position is partially or fully closed based on the chosen method (percentage or RR) above the entry price.

These calculations are crucial for managing risk and optimizing profitability in the strategy.

⍺: BE/TP type (%/RR) | Σ: how many RR/% above the current price

-----

What's the ADR filter? What does it do? What are the underlying calculations?

The Average Day Range (ADR) measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

The period of the ADR filter used in this strategy is tied to the same period you've used for your initial stop-loss.

Users can define the minimum ADR they want to be met before the script looks for entry conditions.

ADR Bias Filter:

- Compares the current bar ADR with the ADR (Defined by user):

- If the current ADR is higher, it indicates that volatility has increased compared to ADR (DbU).(⬆)

- If the current ADR is lower, it indicates that volatility has decreased compared to ADR (DbU).(⬇)

Calculations:

1. Calculate ADR:

- Average the high prices over the specified period.

- Average the low prices over the same period.

- Find the difference between these average values in %.

2. Current ADR vs. ADR (DbU):

- Calculate the ADR for the current bar.

- Calculate the ADR (DbU).

- Compare the two values to determine if volatility has increased or decreased.

By using the ADR filter, the strategy ensures that trades are only taken in favorable market conditions where volatility meets the user's defined threshold, thus optimizing entry conditions and potentially improving the overall performance of the strategy.

>: Minimum required ADR for entry | %: Current ADR comparison to ADR of 14 days ago.

-----

What's the probability filter? What are the underlying calculations?

The probability filter is designed to enhance trade entries by using buyside liquidity and probability analysis to filter out unfavorable conditions.

This filter helps in identifying optimal entry points where the likelihood of a profitable trade is higher.

Calculations:

1. Understanding Swing highs and Swing Lows

Swing High: A Swing High is formed when there is a high with 2 lower highs to the left and right.

Swing Low: A Swing Low is formed when there is a low with 2 higher lows to the left and right.

2. Understanding the purpose and the underlying calculations behind Buyside, Sellside and Equilibrium levels.

3. Understanding probability calculations

1. Upon the formation of a new range, the script waits for the price to reach and tap into equilibrium or the 50% level. Status: "⏸" - Inactive

2. Once equilibrium is tapped into, the equilibrium status becomes activated and it waits for either liquidity side to be hit. Status: "▶" - Active

3. If the buyside liquidity is hit, the script adds to the count of successful buyside liquidity occurrences. Similarly, if the sellside is tapped, it records successful sellside liquidity occurrences.

5. Finally, the number of successful occurrences for each side is divided by the overall count individually to calculate the range probabilities.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

Example - BSL > 55%

-----

What's the range length Filter? What are the underlying calculations?

The range length filter identifies the price distance between buyside and sellside liquidity levels in percentage terms. When enabled, the script only looks for entries when the minimum range length is met. This helps ensure that trades are taken in markets with sufficient price movement.

Calculations:

Range Length (%) = ( ( Buyside Level − Sellside Level ) / Current Price ) ×100

Range Bias Identification:

Bullish Bias: The current range price has broken above the previous external swing high.

Bearish Bias: The current range price has broken below the previous external swing low.

Example - Range length filter is enabled | Range must be above 1%

>: Minimum required range length for entry | %: Current range length percentage in a (Bullish/Bearish) range

-----

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

Increased Flexibility: The filter provides increased flexibility, allowing traders to adapt the strategy to their specific needs and preferences.

Example - Day filter | Session Filter

θ: Session time | Exchange time-zone

-----

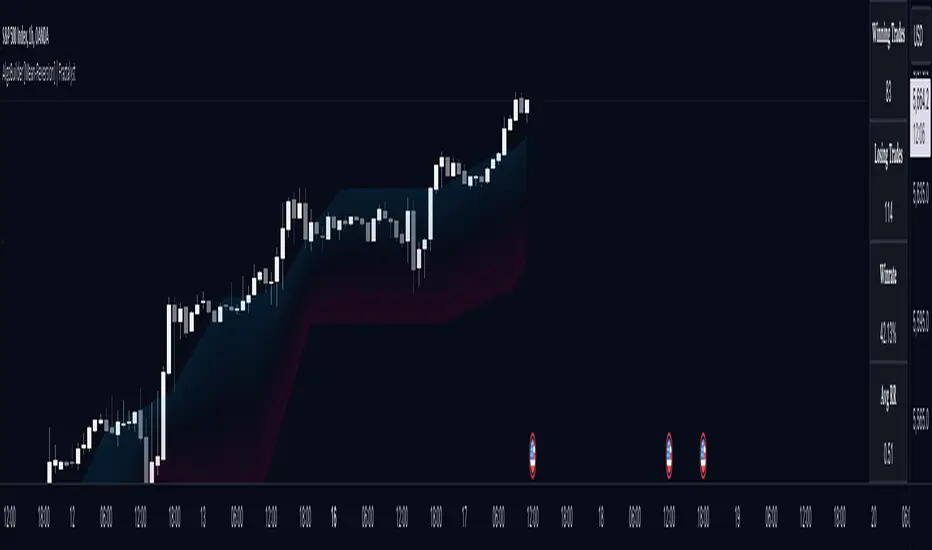

What tables are available in this script?

Table Type:

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- OFF: Hides the performance table.

Profit Color:

- Allows users to set the color for representing profit in the performance table, helping to quickly distinguish profitable periods.

Loss Color:

- Allows users to set the color for representing loss in the performance table, helping to quickly identify loss-making periods.

These customizable tables provide traders with flexible and detailed performance analysis, aiding in better strategy evaluation and optimization.

-----

User-input styles and customizations:

To facilitate studying historical data, all conditions and rules can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

-----

How to Use This Algobuilder to Create a Profitable Edge and System:

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker or prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 100 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade value is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

Automation:

- Once you’re confident in your strategy, you can use the automation section to connect the algorithm to your broker or prop firm.

- Trade a fully automated and backtested trading strategy, allowing for hands-free execution and management.

-----

What makes this strategy original?

1. Incorporating direct integration of probabilities into the strategy.

2. Utilizing built-in market structure-based moving averages across various timeframes.

4. Offering both investing and trading strategies, facilitating optimization from different perspectives.

5. Automation for efficient execution.

6. Providing a summary table for instant access to key parameters of the strategy.

-----

How to use automation?

For Traders:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Enter your PineConnector License ID in the designated field.

3. Specify the desired risk level.

4. Provide the Metatrader symbol.

5. Check for chart updates to ensure the automation table appears on the top right corner, displaying your License ID, risk, and symbol.

6. Set up an alert with the strategy selected as Condition and the Message as {{strategy.order.alert_message}}.

7. Activate the Webhook URL in the Notifications section, setting it as the official PineConnector webhook address.

8. Double-check all settings on PineConnector to ensure the connection is successful.

9. Create the alert for entry/exit automation.

For Investors:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Choose "Investing" in the user-input settings.

3. Create an alert with a specified name.

4. Customize the notifications tab to receive alerts via email.

5. Buying/selling alerts will be triggered instantly upon entry or exit order execution.

-----

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

ابحث في النصوص البرمجية عن "the strat"

Strategy - Plus / Connectable [Azullian]Discover the advanced capabilities of Strategy Plus, an essential component of the connectable indicator system designed for fast-paced strategy testing, visualization, and building within TradingView. This enhanced version of our foundational connectable strategy indicator seamlessly integrates with all connectable indicators . By utilizing the TradingView input source as a signal connector , it facilitates the linking of indicators to form a cohesive strategy. Each connectable indicator within the system sends signal weight to the next node, culminating in a comprehensive strategy that incorporates advanced customization options, sophisticated signal interpretation, and elaborate backtest labeling. Strategy Plus stands out by offering improved position management and extensive alert messaging capabilities, ensuring effective strategy refinement and backend integration.

█ DISTINCTIVE FEATURES

The Connectable Strategy Plus enhances risk mitigation within the connectable system through its advanced features and capabilities:

• Refined Signal Input Management: Tailor and precisely connect up to two signal filters with enhanced input flexibility, gain control, and strategic direction settings.

• Strategic Position Investment Control: Optimize positioning with versatile investment bases, custom investment percentages, and direction-specific investments for effective risk management.

• Advanced Exit Stop Loss Configuration: Implement custom stop loss tactics with diverse base modes and trailing options for tailored risk management.

• Strategic Exit Take Profit Settings: Apply precision-driven take profit strategies with various calculation modes and dynamic trailing functionality.

• Calibrated Entry Position Allocation: Optimize investment distribution for entry positions, including DCA and BRO trades, for strategic market response.

• Refined Order Setting Customization: Ensure exchange compliance with adjustable order settings, enhancing backtest accuracy and strategy reliability.

• Comprehensive Condition Settings: Define precise conditions for strategy execution, including date range filtering and order/loss limitations.

• Intuitive Visualization: Enhance strategy clarity with customizable visual elements and trade visualization features.

• Advanced Alert Configurations: Stay informed with comprehensive and customizable alerts for effective backend integration.

• Backend Integration With JSON Format: Leverage elaborate and structured data in JSON format for advanced analytics, enhancing decision-making and strategy optimization outside TradingView.

Let's review the separate parts of this indicator.

█ STRATEGY INPUTS

We've provided 2 inputs for connecting a signal filter or indicators or chains (1→, 2→) which are all set to 'Close' by default.

An input has several controls:

• Enable disable: Toggle the entire input on or off

• Input: Connect indicators or signal filter here, choose indicators with a compatible : Signal connector.

• G - Gain: Increase or reduce the strength of the incoming signal by a factor.

• SM - Signal Mode: Choose a trading direction compatible with the settings in your signal filter

• XM - Exit Mode: Determine when to allow to exit your open trade

○ Always: Doesn't take the restrictions into account, this ignores all the settings chosen in ML or MP

○ Restricted: Use both ML and MP conditions

○ Loss: Use the ML condition only, for example: Position will be exited and the exit signal will be allowed only when the loss exceeds the ML parameter

○ Profit: Use the MP condition only for example: Exits will only be allowed when the profit of the position exceeds the condition of the MP parameter

█ POSITION INVESTMENT

Determine the percentage of your trading budget you would like to use in each position based on the strategy's profit or loss.

• LINVB - Loss Investment Base: Choose which base to use to determine the investment percentage when the strategy is in a loss.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• LINV% - Loss Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in loss, and a initial capital of $100, and the investment base is set to equity with a percentage of 50%, your investment will be 50% of $90, $45.

• PINVB - Profit Investment Base: Choose which base to use to determine the investment percentage when the strategy is in profit.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• PINV% - Profit Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in profit, and an initial capital of $100, and the investment base is set to equity with a percentage of 100%, your investment will be 100% of $110, $110.

• XINVB - Custom Profit Investment Base: Choose which base to use to determine the investment percentage when the strategy is above a custom profit threshold (XT).

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• XINV% - Custom Profit Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 100% in profit, exceeding the XT threshold of 50%, and an initial capital of $100, and the investment base is set to equity with a percentage of 50%, your investment will be 50% of $200, $100.

• XT% - Custom Profit Threshold: Determine how much profit triggers these custom profit investment settings.

• ELIB% - Entry Long Investment Base: Following previous settings, you can further restrict the investment according to the long trading direction.

○ For instance, if the previous calculation resulted in $45 to be used as an investment, and you've set the ELIB% to 50%, your long position will use 50% of $45, which is $22.5.

• ESIB% - Entry Short Investment Base: Following previous settings, you can further restrict the investment according to the short trading direction.

○ For example, if the previous calculation resulted in $45 to be used as an investment, and you've set the ESIB% to 50%, your short position will use 50% of $45, which is $22.5.

• RISK% - Risk Percentage:

○ Determine how much of the calculated position investment is at risk when the stop-loss is hit.

- For example, 1% of $45 represents a maximum loss of $0.45.

○ Risk percentage works together with the stop loss and the max leverage.

• MXLVG - Maximum Leverage:

○ Investigate the trading rules for your trading pair and use the maximum allowed amount of leverage.

○ To determine the number of contracts to be bought or sold, considering the stop loss and the specified risk percentage, the maximum leverage available will constrain the amount of leverage utilized to ensure that the maximum risk threshold is not exceeded. For instance, suppose the stop loss is set at 1%, and the risk percentage is defined as 10%. Initially, the calculated leverage to be used would be 10. However, if there is a maximum leverage cap set at 5, it would constrain the calculated leverage of 10 to adhere to the maximum limit of 5.

█ EXIT STOP LOSS

Determine the Stop Loss price based on your selected configuration.

As the stop loss is an integral part of the ordered contracts calculation used in conjunction with the Risk and Max leverage, you'll always need to provide a stop loss price.

• SLLB - Stop Loss Long Base: Choose a stop loss mode for calculating stop loss prices in long positions.

○ Risk: Determines the price using the Risk parameter (RISK%) and maximum leverage (MXLVG). In this case, SLLB% will not have any impact.

○ Price Entry + Offset: Calculates the stop loss price based on a offset percentage (SLLB%) from the entry price of the position.

○ Source: Computes the stop loss price based on an external indicator defined in SLLSRC.

- If this results in an invalid price, the calculation will revert to using the price entry + offset.

○ Source + Offset: Determines the stop loss price based on a positive or negative offset percentage (SLLB%) from an external indicator defined in SLLSRC.

- If this results in an invalid price, the calculation will fall back to using the price entry + offset.

• SLLB% - Stop Loss Long Base Percentage: Define an offset percentage that will be applied in the price entry + offset and source + offset stop loss modes.

• SLLSRC - Stop Loss Long Source: Connect an external indicator as the source for stop loss (only those providing price values eg: bollinger bands, moving averages...).

• SLLT - Stop Loss Long Trailing:

○ Fixed: The initial stop loss will be kept and no trailing stop loss will be applied.

○ Trail Stop: Takes into account all settings defined in SLLB and SLLB% and recalculates them with each candle.

- If a better stop loss is computed, it replaces the existing stop loss. In this mode SLLT% will be disregarded.

○ Trail Stop till BE: Similar to trailing stop mode, but it stops trailing when the stop loss reaches the break-even point.

○ Trail Stop from BE: Similar to trailing stop mode, but it starts trailing when the stop loss reaches the break-even point.

○ Trail Price: Computes the trailing stop loss price based on an offset percentage (SLLT%) from the closing price of the current candle.

- If a better stop loss price is calculated, it will be set as the new stop loss price.

○ Trail Price till BE: Similar to the Trail Price mode, but it stops trailing when the stop loss reaches the break-even point.

○ Trail Price from BE: Similar to Trail Price mode, but it starts trailing when the stop loss reaches the break-even point.

○ Trail Incr: Adapts the trailing stop loss price based on the offset percentage (SLLT%).

- Each price change in favor of your position will incrementally adapt the trailing stop loss with SLLT%.

○ Trail Incr till BE: Similar to the Trail Incr mode, but it stops trailing when the stop loss reaches the break-even point.

• SLLT% - Stop Loss Long Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

• SLSB - Stop Loss Short Base: Functions similarly to SLLB but for short positions.

• SLSB% - Stop Loss Short Base Percentage: Functions similarly to SLLB% but for short positions.

• SLSSRC - Stop Loss Short Source: Functions similarly to SLLSRC but for short positions.

• SLST - Stop Loss Short Trailing: Functions similarly to SLLT but for short positions.

• SLST% - Stop Loss Short Trailing Percentage: Functions similarly to SLLT% but for short positions.

█ EXIT TAKE PROFIT

Determine the Take Profit price based on your selected configuration.

• TPLB - Take Profit Long Base: Choose a take profit mode for calculating take profit prices in long positions.

○ Reward: Determines the take profit price using the Risk parameter (RISK%) and the calculated Stop Loss price and the set reward percentage (TPLB%).

- For example: Risk 1%, Calculated Stop loss price: $90, Entry price: $100, Reward (TPLB%): 2%, will result in a take profit price on $120.

○ Price Entry + Offset: Calculates the take profit price based on a offset percentage (TPLB%) from the entry price of the position.

- For example: Entry price: $100, Offset (TPLB%): 2%, will result in a take profit price on $102.

○ Source: Computes the take profit price based on an external input from another indicator defined in TPLSRC.

- If this results in an invalid price, the calculation will revert to using the price entry + offset.

○ Source + Offset: Determines the take profit price based on a positive or negative offset percentage (TPLB%) from an external indicator inpuy defined in TPLSRC.

- If this results in an invalid price, the calculation will fall back to using the price entry + offset.

• TPLB% - Take Profit Long Base Percentage: Define an offset percentage that will be applied in the price entry + offset and source + offset take profit modes.

• TPLSRC - Take Profit Long Source: Choose to connect an external indicator as the source for take profit (of course only those which provide price values eg: bollinger bands, moving averages... but not oscillators).

• TPLT - Take Profit Long Trailing:

○ Fixed: The initial take profit will be kept and no trailing take profit will be applied.

○ Trail Profit: Takes into account all settings defined in TPLB and TPLB% and recalculates them with each candle.

- If an applicable take profit is computed, it replaces the existing take profit. In this mode TPLT% will be disregarded.

○ Trail Profit till BE: Similar to trailing profit mode, but it stops trailing when the take profit reaches the break-even point.

○ Trail Profit from BE: Similar to trailing profit mode, but it starts trailing when the take profit reaches the break-even point.

○ Trail Price: Computes the trailing take profit price based on an offset percentage (TPLT%) from the closing price of the current candle.

- If an applicable take profit price is calculated, it will be set as the new take profit price.

○ Trail Price till BE: Similar to the Trail Price mode, but it stops trailing when the take profit reaches the break-even point.

○ Trail Price from BE: Similar to Trail Price mode, but it starts trailing when the take profit reaches the break-even point.

○ Trail Incr: Adapts the trailing take profit price based on the offset percentage (TPLT%). Each price change against your position will incrementally adapt the trailing take profit with TPLT%.

○ Trail Incr till BE: Similar to the Trail Incr mode, but it stops trailing when the take profit reaches the break-even point.

• TPLT% - Take Profit Long Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

• TPSB - Take Profit Short Base: Functions similarly to TPLB but for short positions.

• TPSB% - Take Profit Short Base Percentage: Functions similarly to TPLB% but for short positions.

• TPSSRC - Take Profit Short Source: Functions similarly to TPLSRC but for short positions.

• TPST - Take Profit Short Trailing: Functions similarly to TPLT but for short positions.

• TPST% - Take Profit Short Trailing Percentage: Functions similarly to TPLT% but for short positions.

█ ENTRY INVESTMENT DISTRIBUTION

Based on your position investment calculation you can distribute the position investment accross the initial opening trade of the position (SIG%) or the follow up Dollar Cost Averaging (DCA%) or Break Out (BRO%) trades.

For example: SIG%: 10%, DCA%: 45%, BRO%: 45% and the calculated Position Investment is $100, then the initial trade will receive $10, DCA will receive $45, and BRO will receive $45 to work with. Disable BRO and or DCA by setting them to 0%. Keep in mind that the sum of SIG, BRO and DCA may not exceed 100%.

• SIG% - Initial order investment percentage based on the signal: The percentage of the position investment distributed over normal trades.

• DCA% - Dollar Cost Averaging investment percentage: The percentage of the position investment distributed to DCA trades.

• BRO% - Break Out investment percentage: The percentage of the position investment distributed to BRO trades.

█ ENTRY DCA

DCA (Dollar-Cost Averaging) is a risk mitigation strategy where the allocated DCA% budget from the Entry Investment Distribution is distributed among x levels (DCA#) based on calculated prices (DPLM) and order sizes (DOSM), when prices move against your position.

• DCA# - Maximum DCA levels: Set the maximum number of DCA levels.

• DPLM - DCA Price Level Mode: Choose a price level mode that determines at which prices the additional purchases are distributed:

○ Linear: Entry prices are evenly spaced at regular intervals.

○ QuadIn: Entry prices are front-loaded, with more at the beginning and fewer later.

○ QuadOut: Entry prices are back-loaded, with fewer at the beginning and more later.

○ QuadInOut: Entry prices start front-loaded, then become back-loaded.

○ CubicIn: Similar to QuadIn but with a smoother front-loaded distribution.

○ CubicOut: Similar to QuadOut but with a smoother back-loaded distribution.

○ ExpoIn: Entry prices are exponentially increasing, starting small and growing.

○ ExpoOut: Entry prices are exponentially decreasing, starting large and reducing.

○ ExpoInOut: Entry prices start exponentially increasing, then decrease exponentially.

• DOSM - DCA Order Size Mode: Choose a DCA budget distribution mode for order sizes:

○ Linear: Order sizes are evenly spaced at regular intervals.

○ QuadIn: Order sizes are front-loaded, with larger orders at the beginning and smaller ones later.

○ QuadOut: Order sizes are back-loaded, with smaller orders at the beginning and larger ones later.

○ QuadInOut: Order sizes start front-loaded and transition to back-loaded.

○ CubicIn: Similar to QuadIn but with a smoother front-loaded distribution of order sizes.

○ CubicOut: Similar to QuadOut but with a smoother back-loaded distribution of order sizes.

○ ExpoIn: Order sizes exponentially increase, starting small and growing.

○ ExpoOut: Order sizes exponentially decrease, starting large and reducing.

○ ExpoInOut: Order sizes start exponentially increasing, then decrease exponentially.

For a visual representation of the price or order size distribution modes, refer to online easing curves.

█ ENTRY BRO

BRO (Break Out) is a risk mitigation strategy where the allocated BRO% budget from the Entry Investment Distribution is distributed among x levels (BRO#) based on calculated prices (BPLM) and order sizes (BOSM), when prices move in favor of your position.

• BRO# - Maximum BRO levels: Set the maximum number of BRO levels.

• BPLM - BRO Price Level Mode: Choose a price level mode that determines at which prices the additional purchases are distributed:

○ Distribution easing modes work similar as the DCA easing modes.

• BOSM - BRO Order Size Mode: Choose a BRO budget distribution mode for order sizes:

○ Distribution easing modes work similar as the DCA easing modes.

█ ORDER SETTINGS

Fine-tune accuracy to match your exchange's trading constraints, enhancing backtest precision with these settings, default settings are least restrictive for crypto trading pairs.

• MINP - Mininmum Position Notional Value: Exchange-defined minimum notional value for positions:

○ Calculated based on your exchange's rules and is the minimum total value your position must hold to meet their requirements It is calculated by multiplying Quantity with price and leverage.

○ It helps ensure your trades align with your exchange's standards.

• MAXP - Maximum Position Notional Value: Exchange-defined maximum notional value for positions:

○ Similar to MINP, this value is calculated based on your exchange's rules and represents the maximum total value allowed for your position.

• MINQ - Mininmum Order Quantity: Least permissible order quantity based on exchange rules:

○ This is the smallest quantity of an asset that your exchange allows you to trade in a single order.

• MAXQ - Maximum Order Quantity: Highest permissible order quantity according to exchange rules:

○ Opposite of MINQ, this is the largest quantity of an asset you can trade in a single order as defined by your exchange.

• DECP - Decimals in Order Price: Allowed decimal places in order prices as per exchange specifications:

○ This value specifies the number of decimal places you can use when specifying the price of an order.

• DECQ - Decimals in Order Quantity: Permitted decimal places in order quantities according to exchange specifications:

○ Similar to DECP, this value indicates the number of decimal places you can use when specifying the quantity of an asset in an order.

█ STRATEGY CONDITIONS

Specify when the strategy is permitted to execute trades.

• DATE: Enable the Date Range filter to restrict entries to a specific date range.

○ START: Set a start date and hour to commence trading.

○ END: Set an end date and hour to conclude trading within the defined range.

• IDO - Maximum Intraday Orders: Limit the number of orders the strategy can place within a single trading day. Upon reaching this limit, the strategy temporarily halts further entries for the day.

• DL% - Maximum Intraday Loss%: Set a threshold for the maximum allowable intraday loss as a percentage of equity. When exceeded, the strategy temporarily suspends trading for the day.

• CLD - Maximum Consecutive Loss Days: Define the maximum number of consecutive days the strategy can incur losses. Upon reaching this limit, the strategy halts trading and avoids new entries.

• DD% - Maximum Drawdown: Specify the maximum permissible drawdown as a percentage of equity. If this limit is met, the strategy halts trading and refrains from placing additional entries.

• TP% - Total Profit %: Establish a target for the total profit percentage the strategy aims to achieve. Once this target is attained, the strategy halts trading and refrains from initiating new entries.

• TL% - Total Loss %: Define a limit for the total loss percentage relative to the initial capital. If this limit is exceeded, the strategy discontinues trading and refrains from placing further entries.

■ VISUALS

• LINE: Activate a colored dashed diagonal line to visually connect the entry and exit points of positions.

• SLTP: Enable visualization of stop loss, take profit, and break-even levels.

• PNL: Enable Break-Even and Close Lines along with a colored area in between to visualize profit and loss.

• ☼: Brightness % : Adjust the opacity of the plotted trading visuals.

• P - Profit Color : Choose the color for profit-related elements.

• L - Loss Color: Choose the color for loss-related elements.

• B - Breakeven Color : Select the color for break-even points.

• EL - Long Color: Specify the color for long positions.

• ES - Short Color: Specify the color for short positions.

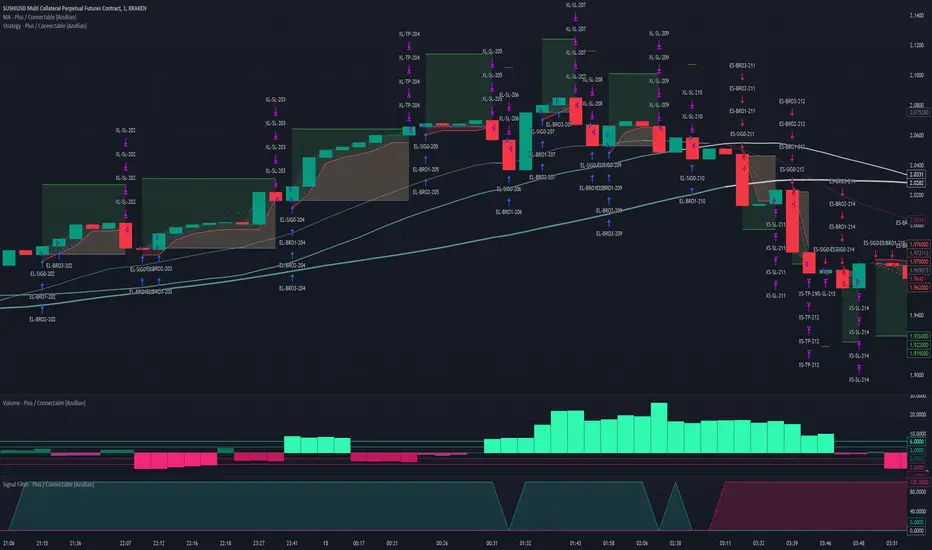

• TRADE LABELING: For better analysis we've labeled all entries and exits conform with the type of order your strategy has executed, some examples:

○ EL-SIG0-124: Enter Long - Signal 0 - Position 124

○ EL-BRO1-130: Enter Long - BRO1 - Position 130

○ EL-BRO2-130: Enter Long - BRO2 - Position 130

○ ES-DCA1-140: Enter Short - DCA1 - Position 140

○ XS-DCA2-140: Exit Short - DCA2 - Position 140

○ XL-TP-150: Exit Long - Take Profit - Position 150

○ XS-TP-154: Exit Short - Take Profit - Position 154

○ XL-SL-160: Exit Long - Stop Loss - Position 160

○ XS-SL-164: Exit Short - Stop Loss - Position 164

○ XS-CND-165: Exit Short - Strategy Condition - Max intraday loss - Position 165

■ ALERT SETTINGS

For developers and those who wish to integrate TradingView alerts into their backend systems, we offer comprehensive labeling options.

• ALID: A unique identifier you've assigned to your alert.

• NAME: A structured name you've given to this strategy.

• LAYOUT: The layout key of the strategy, allowing direct chart linking from your backend.

• SYMBOL: The symbol on which the strategy operates.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• TICK: The ticker for the strategy.

• CHART: The chart parameter containing the timeframe.period and timeframe.multiplier.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• BAR: Includes bar information in the alert message.

• STRATEGY: Adds strategy inputs to the alert message.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• PERFORMANCE: Incorporates strategy performance data into the alert message.

• SIGNAL: Appends received signal weights (EL, XL, ES, XS) to the alert message.

• ORDERS: Includes order details in the alert message.

• TAGS: Adds up to 6 tags and their corresponding values to the alert message.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

Of course we can't neglect letting you in on how this juicy JSON would look (without the // comments):

{

"id": 20726, // Message Id

"t": "2023-11-01T10:35:00Z", // Message Time

"al": { // Alert

"id": "639bfa9a-5f01-4031-8880-7ec01e972055", // Alert Id

"n": "TEST04", // Name

"l": "ABC123" // Layout

},

"sym": { // Symbol

"typ": "crypto", // Type

"r": "DOGEUSD.PM", // Root

"pre": "KRAKEN", // Prefix

"tc": "DOGEUSD.PM", // Ticker

"bc": "DOGE", // BaseCurrency

"c": "USD", // Currency

"d": "DOGEUSD Multi Collateral Perpetual Futures Contract", // Description

"mtc": 0.000001, // MinTick

"pv": 1, // PointValue

"ct": "PF_DOGEUSD" // CustomTicker

},

"ch": { // Chart

"pd": "1", // Period

"mul": 1 // Multiplier

},

"bar": { // Bar

"id": 20725, // Index

"t": "2023-11-01T10:33:00Z", // Time

"o": 0.066799, // Open

"h": 0.066799, // High

"l": 0.066799, // Low

"c": 0.066799, // Close

"v": 2924 // Vol

},

"strat": { // Strategy

"n": "Strategy - Plus / Connectable ", // Name

"sig": { // Signal

"c1e": true, // Connector1Enabled

"c1s": 500500.500501, // Connector1Source

"c1g": 1, // Connector1Gain

"c2e": false, // Connector2Enabled

"c2s": 0.067043, // Connector2Source

"c2g": 1, // Connector2Gain

"sm": "Swing (EL, ES)", // SignalMode

"xm": "Always", // ExitMode

"mlp": 0.01, // ExitModeMinPercLoss

"mpp": 0.01 // ExitModeMinPercProfit

},

"inv": { // Investment

"lb": "Equity", // LossBase

"lp": 50, // LossPerc

"pb": "Equity", // ProfitBase

"pp": 100, // ProfitPerc

"pcb": "Equity", // ProfitCustomBase

"pcp": 100, // ProfitCustomPerc

"pct": 10000, // ProfitCustomThreshold

"elp": 100, // LongPerc

"esp": 100, // ShortPerc

"rsk": 1, // MaxRisk

"lvg": 10 // MaxLeverage

},

"sl": { // StopLoss

"lb": "Price Entry + Offset", // LongBase

"lp": 0.2, // LongPerc

"lsrc": 0.067043, // LongSource

"lt": "Trail Stop", // LongTrailMode

"ltp": 0.2, // LongTrailPerc

"sb": "Price Entry + Offset", // ShortBase

"sp": 0.2, // ShortPerc

"ssrc": 0.067043, // ShortSource

"st": "Trail Stop", // ShortTrailMode

"stp": 0.2 // ShortTrailPerc

},

"tp": { // TakeProfit

"lb": "Price Entry + Offset", // LongBase

"lp": 1, // LongPerc

"lsrc": 0.067043, // LongSource

"lt": "Fixed", // LongTrailMode

"ltp": 1, // LongTrailPerc

"sb": "Price Entry + Offset", // ShortBase

"sp": 1, // ShortPerc

"ssrc": 0.067043, // ShortSource

"st": "Fixed", // ShortTrailMode

"stp": 1 // ShortTrailPerc

},

"dis": { // Distribution

"sigp": 10, // SignalPerc

"dcap": 0, // DCAPerc

"brop": 90 // BROPerc

},

"dca": { // DCA

"lvl": 3, // Levels

"pl": "linear", // ModePriceLevel

"os": "linear" // ModeOrderSize

},

"bro": { // BRO

"lvl": 3, // Levels

"pl": "expoIn", // ModePriceLevel

"os": "cubicOut" // ModeOrderSize

},

"ord": { // OrderSettings

"pmin": 5, // PNVMin

"pmax": 30000000, // PNVMax

"qmin": 0, // QtyMin

"qmax": 1000000000, // QtyMax

"dp": 6, // DecPrice

"dq": 6 // DecQty

},

"cnd": { // Conditions

"de": true, // DateRangeEnabled

"start": "2023-11-01T10:30:00Z", // StartTime

"end": "2024-12-31T23:30:00Z", // EndTime

"idoe": false, // MaxIntradayOrdersEnabled

"ido": 100, // MaxIntradayOrders

"dle": false, // MaxIntradayLossEnabled

"dl": 10, // MaxIntradayLossPerc

"clde": false, // MaxConsLossDaysEnabled

"cld": false, // MaxConsLossDays

"dde": false, // MaxDrawdownEnabled

"dd": 100, // MaxDrawdownPerc

"mpe": false, // MaxProfitEnabled

"mp": 200, // MaxProfitPerc

"mle": false, // MaxLossEnabled

"ml": -50 // MaxLossPerc

}

},

"perf": { // Performance

"ic": 1000, // InitialCapital

"eq": 1000, // Equity

"np": 0, // NetProfit

"op": 0, // OpenProfit

"ct": 0, // ClosedTrades

"ot": 0, // OpenTrades

"p": "FLAT", // MarketPosition

"ps": 0, // MarketPositionSize

"pp": "FLAT", // PreviousMarketPosition

"pps": 0 // PreviousMarketPositionSize

},

"sig": { // Signal

"el": 0, // EL

"xl": 0, // XL

"es": 6, // ES

"xs": 0 // XS

},

"ord": ,

"tag":

}

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with signals and a signal filter

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, monitor, or strategy .

Let's connect the Strategy - Plus to a connectable signal filter and connectable indicators :

1. Load all relevant indicators

• Load MA - Plus / Connectable

• Load Signal filter - Plus / Connectable

• Load Strategy - Plus / Connectable

2. Signal Filter Plus: Connect the MA - Plus to the Signal Filter

• Open the signal filter settings

• Choose one of the five input dropdowns (1→, 2→, 3→, 4→, 5→) and choose : MA - Plus / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter settings if needed

• The default filter mode for the trading direction is SWING, and is compatible with the default settings in the strategy and indicators.

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold is 'ABOVE' Threshold 1 (TH1) and Threshold 2 (TH2), both set at 5. This allows each occurrence to score, as the default score is 1 point above the threshold.

5. Strategy Plus: Connect one of the strategy plus inputs to the signal filters signal connector in the strategy settings

• Select a strategy input → and select the Signal filter - Plus: Signal connector

6. Strateg Plus: Enable filter compatible directions

• As the default setting of the filter is SWING, we should also set the SM (Strategy mode) to SWING.

7. Strateg Plus: You're ready to start optimizing

• Dive into all parameters and start optimizing your backtesting results.

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

• Layout and Abbreviations: Abbreviations streamline structure and input identification. Although they may seem complex initially, inline tooltips provide explanations, facilitating quick acclimatization.

• Total Trade Limit Error & Date-Time Filter: For deep backtesting, be mindful of the total trade limit. Utilize the date-time filter to narrow the test scope and avoid TradingView order limits.

• Calculation Timeout: Encounter a timeout? Adjust any parameter slightly to restart the calculation process.

• Message Character Limit: To stay within message character limits, consider turning off certain features or setting some to 'once'.

• Direct Indicator-to-Strategy Connection: When connecting an indicator directly to a strategy without thresholds, the strategy will default to long if weights are equally assigned.

• Pyramid Enabling with DCA and BRO: Activate pyramid orders, enabling you to optimize your strategy during Dollar Cost Averaging and Break Out trades.

• Recalculate & Fill Orders Properties: Adjusting these default settings in strategy properties tab may lead to unexpected behavior when backtesting. Approach with caution.

• Optimized for Crypto: Our indicators have been optimized and tested primarily on cryptocurrency markets. Results in other markets may vary.

• Inline Tooltips Documentation: Detailed documentation and guidance are available via inline tooltips for immediate assistance.

• Strategy Settings Margin: Set margin to 1 to be able to apply leverage.

• Styling Panel: Explore the styling panel to disable labels or any other visual cues to reduce clutter on busy charts, enhancing visual clarity and personalization.

• Applying Leverage on Spot Markets: Ensure that maximum leverage on spot markets is configured to 1.

• Unrealistic Order Sizes: Verify that the order book can accommodate your backtested order sizes.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

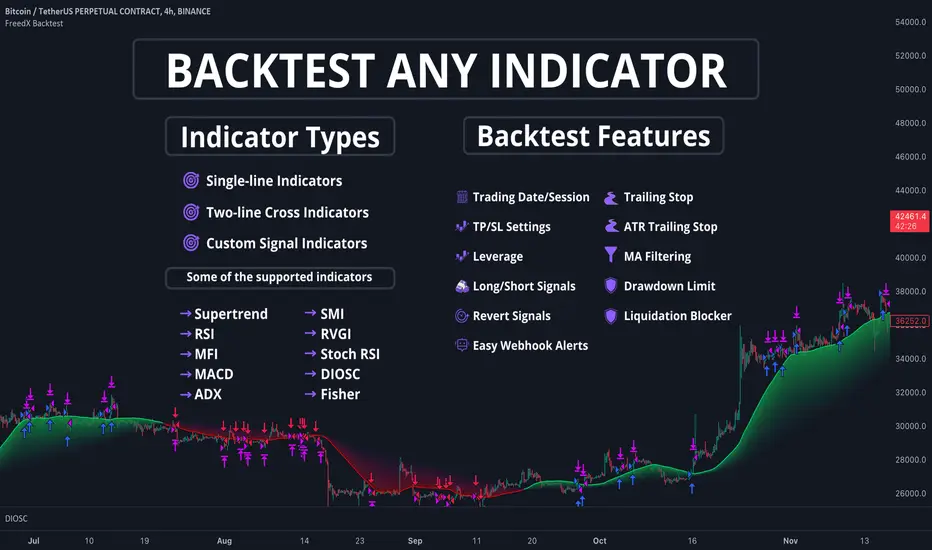

FreedX Backtest█ Our strategy template empowers TradingView users to effortlessly backtest any indicator, enhancing their trading strategy's effectiveness. In addition, users can create automated webhook alerts from the template. This document details our template's features and how to utilize them effectively.

█ TRADE DATE SETTINGS

The Trading Date Settings feature in our TradingView script allows you to refine their backtesting parameters by specifying trading dates and hours. This feature enhances the accuracy of the backtest by aligning it with specific time frames and days, ensuring that the strategy is tested under relevant market conditions.

Features:

⚙️ Enable Trading Between Specific Dates:

🎯 Purpose:

→ Allows you to limit the backtesting of their strategy to a specific date range.

💡 How to Use:

→ Input the Start Date and End Date for the backtest period.

→ The script will execute the strategy only within this specified date range.

⚙️ Enable Trading Between Specific Hours:

🎯 Purpose:

→ Allows you to limit the backtesting of their strategy to a specific hour range.

💡 How to Use:

→ Input the start and end hour for in Trading Session section.

→ The script will execute the strategy only within this specified hour range.

⚙️ Enable Trading on Specified Days of the Week:

🎯 Purpose:

→ Gives you the option to conduct backtesting on selected days of the week, tailoring the strategy to particular market behaviours that may occur on these days.

💡 How to Use:

→ Select the days of the week for the backtest.

→ The script will activate the trading strategy only on these chosen days.

█ BUY/SELL TRIGGER SETTINGS

The Buy/Sell Trigger Settings feature is designed to provide users with flexibility in defining the conditions for 'LONG' and 'SHORT' signals based on various indicator types. This customization is crucial for tailoring strategies to different trading styles and market conditions.

Features:

⚙️ Single-Line Plotted Indicators :

🎯 Purpose:

→ Enables you to select a single-line plotted indicator as a source for backtesting. You can define specific levels to trigger 'LONG' or 'SHORT' signals.

💡 How to Use:

→ Choose a Single-Line Plotted indicator as the source.

→ Set the top and bottom levels for the indicator.

→ The script triggers 'LONG' signals at the bottom level and 'SHORT' signals at the top level.

⚙️ Two-Line Plotted Indicators :

🎯 Purpose:

→ Allows backtesting with two-line cross plot sources. Signals are generated based on the crossover of these lines.

💡 How to Use:

→ Select two lines as 'Source 1' and 'Source 2' for the indicator.

→ The script triggers a 'LONG' signal when 'Source 1' crosses above 'Source 2'.

→ Conversely, a 'SHORT' signal is triggered when 'Source 2' crosses above 'Source 1'.

⚙️ Custom Signals :

🎯 Purpose:

→ This setting enables users to define their own criteria for LONG, SHORT, and CLOSE signals based on custom indicator outputs.

💡 How to Use:

→ Select the custom source for your signals.

→ Define the output values that correspond to each signal type (e.g., “1” for 'LONG', “-1” for SHORT, and “0” for CLOSE).

→ The script will trigger signals according to these custom-defined values.

█ TP/SL SETTINGS

The TP/SL (Take Profit/Stop Loss) Settings feature is designed to give users control over their profit securing and risk mitigation strategies. This feature allows for setting custom TP and SL levels, which can be critical in managing trades effectively.

Features:

Custom TP/SL Levels for Long/Short Signals:

🎯 Purpose:

→ Enables users to set specific percentage levels for Take Profit and Stop Loss on long and short signals.

💡 How to Use:

→ In the TP/SL Settings, input the desired percentage for Take Profit (TP) and Stop Loss (SL).

→ For example, to secure a profit at a 10% price increase on LONG signals, set the “Long TP Percentage” to “10”.

█ STRATEGY SETTINGS

Strategy Settings provide a range of options to customize the trading strategy. These settings include leverage, drawdown limits, position direction changes, and more, allowing users to tailor their strategy to their risk tolerance and market view.

Features:

⚙️ Enable Leverage :

🎯 Purpose:

→ Allows users to apply leverage to their trades.

☢️ Caution:

→ High leverage can significantly increase the risk of liquidation.

→ High leverage and a high stop-loss price may override your fixed stoploss percentage, adjusting the stop-loss to the liquidation price.

💡 How to Use:

→ Set the desired leverage ratio in the Strategy Settings.

⚙️ Enable Drawdown Limit:

🎯 Purpose:

→ Sets a maximum drawdown limit, automatically halting the strategy if this limit is reached, thereby controlling risk.

💡 How to Use:

→ Input the maximum drawdown limit (default: 100, min: 0, max: 100).

⚙️ Enable Reverse Position:

🎯 Purpose:

→ Automatically closes a current position and opens a new one in the opposite direction upon detecting a signal for a market trend change.

🎯 Example:

→ If a LONG signal is received while in a SHORT position, the script will close the SHORT position and open a LONG position.

💡 How to Use:

→ Activate this feature in the Strategy Settings.

⚙️ Enable Spot Mode:

🎯 Purpose:

→ Disables short orders, using short signals only for closing long positions.

💡 How to Use:

→ Select the 'Spot Mode' option in the Strategy Settings.

⚙️ Enable Invert Signals:

🎯 Purpose:

→ Inverts all indicator signals, changing LONG signals to SHORT and vice versa.

💡 How to Use:

→ Opt for the 'Invert Signals' feature in the Strategy Settings.

⚙️ Enable Trailing Stop:

🎯 Purpose:

→ Triggers a trailing stop order on the exchange instead of a standard stop market order.

☢️ Caution:

→ The backtesting of this feature on TradingView may not accurately reflect actual strategy performance due to discrepancies between TradingView and exchange mechanisms.

💡 How to Use:

→ Select 'Trailing Stop' in the Strategy Settings.

█ ADVANCED STRATEGY SETTINGS

Advanced Strategy Settings offer sophisticated methods for managing Stop Loss (SL) and Take Profit (TP) using the Average True Range (ATR). These settings are ideal for traders who want to incorporate volatility into their exit strategies.

Features:

⚙️ Enable ATR Stop Loss:

🎯 Purpose:

→ Automatically sets the Stop Loss price using the Average True Range at the time of entry.

💡 How to Use:

→ Activate 'ATR Stop Loss' to have the SL price calculated based on the current ATR.

⚙️ Enable ATR Take Profit:

🎯 Purpose:

→ Sets the Take Profit price based on the Average True Range at the time of entry.

💡 How to Use:

→ Choose 'ATR Take Profit' for TP price determination using ATR.

⚙️ Enable ATR Trailing Stop:

🎯 Purpose:

→ Dynamically updates the Stop Loss price with each new bar, according to the Average True Range.

💡 How to Use:

→ Activate 'ATR Trailing Stop'.

→ Set the ATR Period to define the number of bars for ATR calculation.

→ Adjust the ATR SL Multiplier to determine the stop loss distance.

→ Modify the ATR TP Multiplier for setting the take profit distance.

█ TREND FILTERING SETTINGS

Trend Filtering Settings are designed to align trading strategies with the prevailing market trend, enhancing the precision of trade entries and exits. These settings utilize moving averages for trend analysis and decision-making.

Features:

⚙️ Enable Trend Filtering:

🎯 Purpose:

→ Limits trades based on moving average trends, blocking short trades in an uptrend and vice versa.

💡 How to Use:

→ Enable 'Trend Filtering'.

→ Set Fast and Slow MA Lengths for trend analysis.

→ Select the Timeframe for moving averages.

→ Choose the Moving Average Type for trend filtering.

🎯 Note:

→ Be cautious with timeframe selections; lower timeframes than the base may cause inconsistencies.

⚙️ Enable Exit on Trend Reversal:

🎯 Purpose:

→ Automatically closes a position when a market trend reversal is detected.

💡 How to Use:

→ Turn on 'Exit on Trend Reversal' in the settings.

⚙️ Enable Trend Drawing On Chart:

🎯 Purpose:

→ Visually represents the trend filter directly on the chart for easy reference.

💡 How to Use:

→ Activate 'Trend Drawing On Chart' to see the trend filter overlaid on the trading chart.

█ AUTOMATED ALERT SETTINGS

Automated Alert Settings are designed to integrate your TradingView script with webhook alerts. These settings allow for enhanced strategy execution and management.

Features:

Enable Webhook Alerts:

🎯 Purpose:

→ Trigger BUY, SELL, CHANGE_DIRECTION or MOVE_STOP_LOSS .

💡 How to Use:

→ Enable 'Webhook Alerts' in the settings.

→ Enter your Strategy ID.

→ Optionally, activate 'Override Allocation Percentage' to bypass the preset allocation percentage.

☢️ Caution:

→ Overriding the allocation percentage may result in trade entry errors due to misalignment between entry cost and available balance.

█ DEBUGGING SETTINGS

Debugging Settings are crucial for users who want to analyze and optimize their strategies. These settings provide tools for visualizing alerts on charts and accessing detailed data outputs.

Features:

⚙️ Enable Alert Plotting:

🎯 Purpose:

→ Allows users to visualize trading alerts directly on the chart, aiding in strategy analysis and refinement.

💡 How to Use:

→ Activate 'Alert Plotting' to draw alerts on the chart.

☢️ Caution:

→ It is recommended to disable this feature when creating actual trading alerts, as it can cause latency in signal processing.

⚙️ Enable Debugger Mode:

🎯 Purpose:

→ Facilitates strategy debugging by providing detailed data output in the TradingView Data Window.

💡 How to Use:

→ Turn on 'Debugger Mode' to access real-time data and metrics relevant to your strategy.

█ ADDITIONAL SETTINGS

⚙️ Enable Bar Magnifier

⚙️ Enable Using standard OHLC

Martingale + Grid DCA Strategy [YinYangAlgorithms]This Strategy focuses on strategically Martingaling when the price has dropped X% from your current Dollar Cost Average (DCA). When it does Martingale, it will create a Purchase Grid around this location to likewise attempt to get you a better DCA. Likewise following the Martingale strategy, it will sell when your Profit has hit your target of X%.

Martingale may be an effective way to lower your DCA. This is due to the fact that if your initial purchase; or in our case, initial Grid, all went through and the price kept going down afterwards, that you may purchase more to help lower your DCA even more. By doing so, you may bring your DCA down and effectively may make it easier and quicker to reach your target profit %.

Grid trading may be an effective way of reducing risk and lowering your DCA as you are spreading your purchases out over multiple different locations. Likewise we offer the ability to ‘Stack Grids’. What this means, is that if a single bar was to go through 20 grids, the purchase amount would be 20x what each grid is valued at. This may help get you a lower DCA as rather than creating 20 purchase orders at each grid location, we create a single purchase order at the lowest grid location, but for 20x the amount.

By combining both Martingale and Grid DCA techniques we attempt to lower your DCA strategically until you have reached your target profit %.

Before we start, we just want to make it known that first off, this Strategy features 8% Commission Fees, you may change this in the Settings to better reflect the Commission Fees of your exchange. On a similar note, due to Commission Fees being one of the number one profit killers in fast swing trade strategies, this strategy doesn’t focus on low trades, but the ideology of it may result in low amounts of trades. Please keep in mind this is not a bad thing. Since it has the ability to ‘Stack Grid Purchases’ it may purchase more for less and result in more profit, less commission fees, and likewise less # of trades.

Tutorial:

In this example above, we have it set so we Martingale twice, and we use 100 grids between the upper and lower level of each martingale; for a total of 200 Grids. This strategy will take total capital (initial capital + net profit) and divide it by the amount of grids. This will result in the $ amount purchased per grid. For instance, say you started with $10,000 and you’ve made $2000 from this Strategy so far, your total capital is $12,000. If you likewise are implementing 200 grids within your Strategy, this will result in $12,000 / 200 = $60 per grid. However, please note, that the further down the grid / martingale is, the more volume it is able to purchase for $60.

The white line within the Strategy represents your DCA. As the Strategy makes purchases, this will continue to get lower as will your Target Profit price (Blue Line). When the Close goes above your Target Profit price, the Strategy will close all open positions and claim the profit. This profit is then reinvested back into the Strategy, which may exponentially help the Strategy become more profitable the longer it runs for.